A customer emails asking for their money back. Simple enough, right? But here's where things get tricky: how you handle that request in the next few hours can determine whether you process a quick refund, fight a costly chargeback, or watch a dispute spiral into something that threatens your payment processing entirely.

For SaaS companies, the difference between a refund and a chargeback isn't just semantic. It's the difference between a $50 refund you control and a $50 chargeback that costs you $65 plus hours of documentation work. Get the distinction wrong often enough, and you'll find yourself dealing with dispute monitoring programs that can freeze your ability to accept payments altogether.

This guide breaks down exactly what your support team needs to know: the right words to use, the evidence to save before you need it, and the escalation triggers that protect your business.

The Operational Difference Between Refunds and Chargebacks

Let's start with the basics, because even experienced support teams sometimes blur these lines.

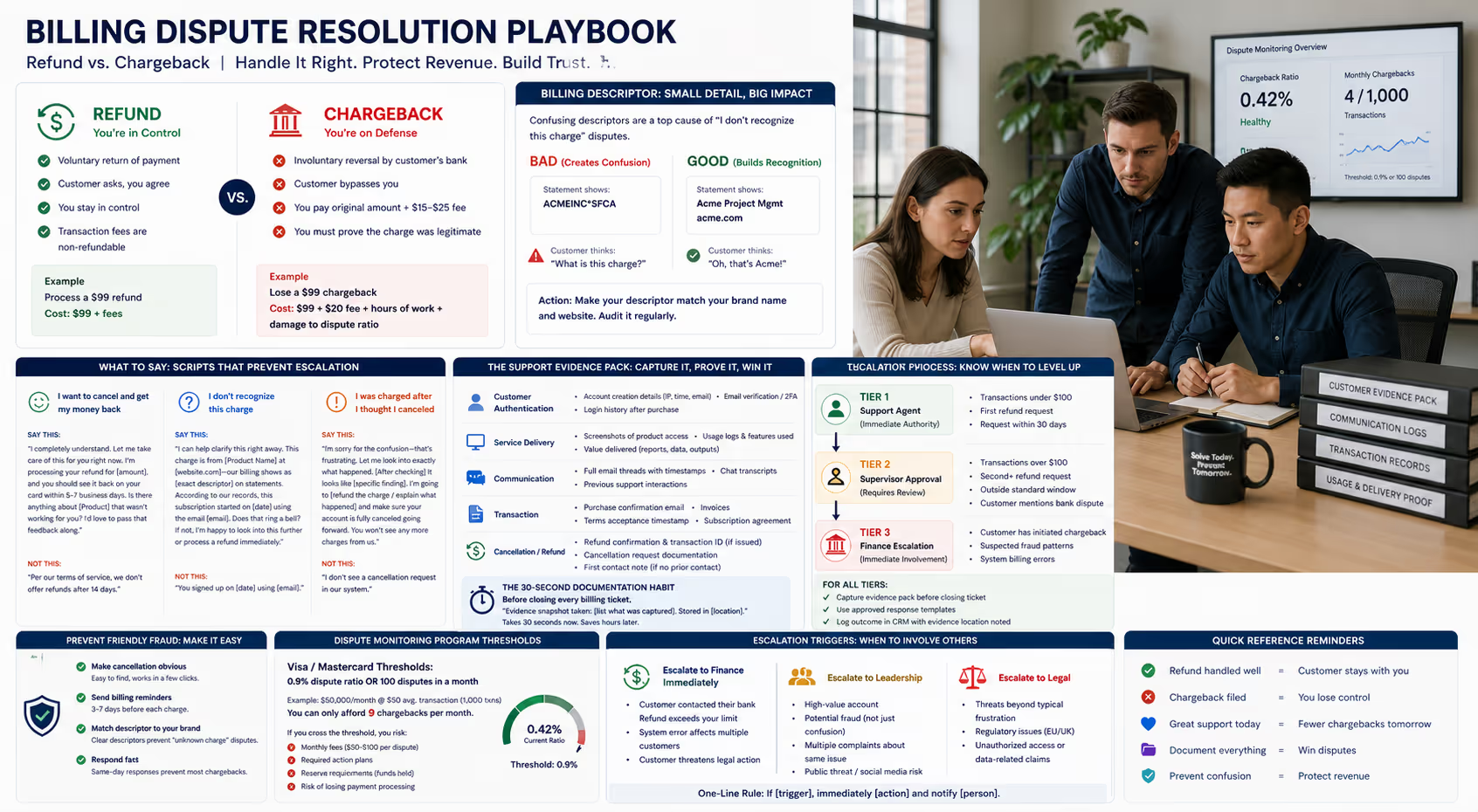

A refund is a voluntary return of payment that you initiate. The customer asks, you agree, money goes back. You stay in control. The transaction cost you already paid doesn't come back, but that's the extent of it.

A chargeback is an involuntary reversal initiated by the customer's bank. The customer bypasses you entirely, contacts their card issuer, and disputes the charge. Now you're on defense. You'll pay the original amount plus a chargeback fee (typically $15-25 per incident), and you'll need to prove the charge was legitimate if you want to fight it [1].

Here's the part that matters for daily support work: a refund request handled well almost never becomes a chargeback. A refund request handled poorly—or ignored—frequently does.

The math is straightforward. Process a $99 refund, and you're out $99 plus whatever transaction fees you originally paid. Lose a $99 chargeback, and you're out $99 plus $20 in fees plus three hours of documentation work plus a black mark on your dispute ratio.

What Your Billing Descriptor Has to Do With Everything

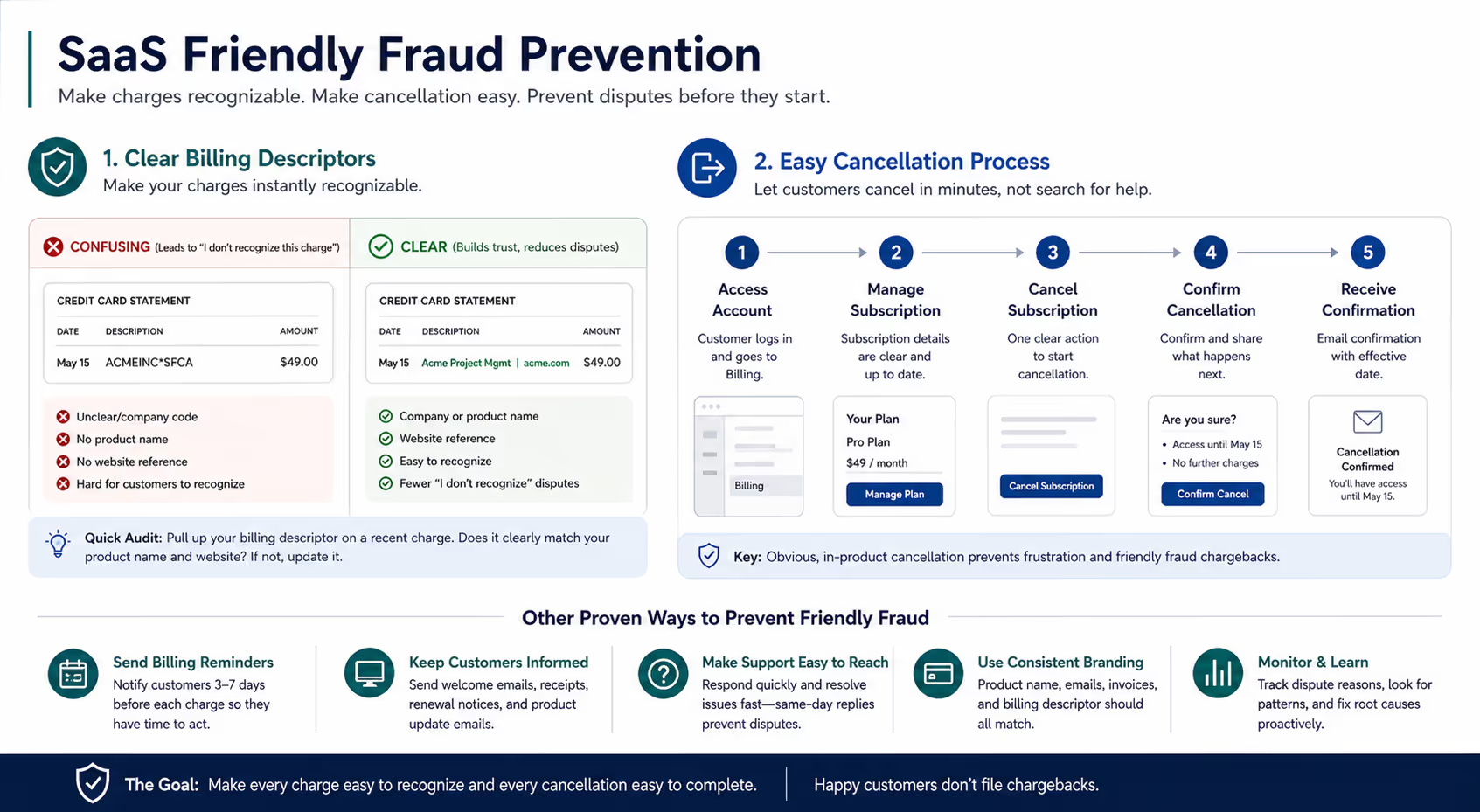

Before we talk about what support should say, let's address the silent cause of "friendly fraud" chargebacks: confusing billing descriptors.

Your billing descriptor is what appears on a customer's credit card statement. If your company is "Acme Project Management" but your billing descriptor shows "ACMEINC*SFCA," you've just created a chargeback waiting to happen [2].

Customers see an unfamiliar charge, don't recognize it, and dispute it with their bank rather than emailing you. That's not malicious fraud—it's confusion that your billing setup created.

Quick audit: Pull up what your billing descriptor actually shows. If it doesn't clearly match your product name or website, fix it before your next support training. This single change can reduce "I don't recognize this charge" disputes significantly.

What Support Should Say: Scripts That Prevent Escalation

The words your team uses in the first response to a billing complaint often determine whether you're processing a refund or fighting a chargeback next month.

For "I want to cancel and get my money back"

Don't say: "Per our terms of service, we don't offer refunds after 14 days."

Do say: "I completely understand. Let me take care of this for you right now. I'm processing your refund for [amount], and you should see it back on your card within 5-7 business days. Is there anything about [Product] that wasn't working for you? I'd love to pass that feedback along."

Why this works: You've resolved the issue before frustration builds. You've given a clear timeline. And you've opened a door for feedback that might reveal a product issue worth fixing.

For "I don't recognize this charge"

Don't say: "You signed up on [date] using [email]."

Do say: "I can help clarify this right away. This charge is from [Product Name] at [website.com]—our billing shows as [exact descriptor] on statements. According to our records, this subscription started on [date] using the email [email]. Does that ring a bell? If not, I'm happy to look into this further or process a refund immediately."

Why this works: You've connected your billing descriptor to your actual product name (solving the recognition problem), provided specifics, and offered immediate resolution.

For "I was charged after I thought I canceled"

Don't say: "I don't see a cancellation request in our system."

Do say: "I'm sorry for the confusion—that's frustrating. Let me look into exactly what happened. [After checking] It looks like [specific finding]. I'm going to [refund the charge / explain what happened] and make sure your account is fully canceled going forward. You won't see any more charges from us."

Why this works: You've acknowledged frustration, investigated before defending, and provided closure.

The Support Evidence Pack: What to Save and When

Here's the part most support teams get wrong: they try to gather evidence after a chargeback arrives. By then, critical information has often been deleted, overwritten, or become inaccessible.

Build your evidence pack at the moment of every billing-related support ticket. Yes, even the ones you resolve with a quick refund.

Your Chargeback Defense Checklist

Save these items immediately when handling any billing complaint:

Customer authentication evidence:

Screenshot of account creation details (IP address, timestamp, email used)

Record of email verification or two-factor authentication

Login history showing product usage after purchase

Service delivery evidence:

Screenshots showing the customer accessed the product

Usage logs (features used, documents created, sessions logged)

Any value delivered (reports generated, data processed)

Communication evidence:

Full email thread with timestamps

Any chat transcripts

Record of previous support interactions

Transaction evidence:

Original purchase confirmation email

Invoice copies

Subscription agreement or terms acceptance timestamp

Cancellation/refund evidence:

If you issued a refund: confirmation email and transaction ID

If they requested cancellation: documentation of when and how it was processed

If no prior contact: note confirming this is first communication

The 30-Second Documentation Habit

Train your team to add this to every billing ticket before closing:

"Evidence snapshot taken: [list what was captured]. Stored in [location]."

This takes 30 seconds now and saves hours later. When a chargeback arrives eight weeks from now, you'll have everything you need in one place.

Friendly Fraud: The Gray Area That Costs You Money

"Friendly fraud" sounds like an oxymoron, but it describes a real and growing problem: customers who receive a legitimate product or service, then dispute the charge anyway [3].

Sometimes this is intentional. More often, it's one of these scenarios:

The customer forgot they signed up

A family member used their card

They didn't realize the trial converted to paid

They couldn't figure out how to cancel

They got frustrated and went straight to their bank

Your support team can prevent most friendly fraud by making these things easier:

Make cancellation obvious. If customers can't find the cancel button, they'll call their bank instead. A clear cancellation process prevents disputes.

Send billing reminders. An email 3-7 days before each charge gives customers a chance to cancel or update payment methods before frustration builds.

Make your billing descriptor match your brand. We covered this earlier, but it bears repeating: unclear descriptors cause chargebacks.

Respond fast. A customer who gets a same-day response rarely files a chargeback. A customer waiting 72 hours for help might.

When to Escalate: The Triggers Your Team Needs to Know

Not every billing complaint stays in support. Here's when to loop in finance, leadership, or legal:

Escalate to finance immediately when:

The customer mentions they've already contacted their bank

The refund amount exceeds your authorization limit

You discover a billing system error affecting multiple customers

The customer threatens legal action

Escalate to leadership when:

The customer is a high-value account (define your threshold)

The situation involves potential fraud (not just confusion)

Multiple complaints about the same issue arrive within a short window

The customer has significant social media reach and expresses intent to post publicly

Escalate to legal when:

The customer makes threats beyond typical frustration

There's a potential regulatory issue (especially for customers in EU/UK)

The dispute involves claims of unauthorized access or data issues

Create a one-line escalation rule: "If [trigger], immediately [action] and notify [person]."

Document these triggers somewhere your whole team can access. When escalation criteria are vague, things fall through cracks.

Dispute Monitoring Program Thresholds: The Numbers That Matter

Here's the business reality your support team should understand: payment processors track your chargeback ratio, and crossing certain thresholds triggers serious consequences [4].

Visa's Dispute Monitoring Program kicks in at 0.9% dispute ratio or 100 disputes in a month. Mastercard's threshold is similar. Once you're in a monitoring program, you face:

Monthly fees ($50-100 per dispute on top of standard fees)

Required action plans

Potential reserve requirements (processors hold a percentage of your revenue)

Risk of losing payment processing entirely

For a SaaS company processing $50,000/month with an average transaction of $50 (1,000 transactions), you can only afford 9 chargebacks per month before hitting monitoring thresholds.

Nine. That's it.

This is why preventing chargebacks through good support isn't just about individual transactions—it's about protecting your ability to accept payments at all.

The Refund-First Philosophy (And When It Makes Sense)

Some SaaS companies have adopted a "refund first, ask questions later" approach. The logic: the cost of fighting chargebacks exceeds the cost of generous refunds.

This makes sense when:

Your average transaction value is relatively low

Your margins can absorb refund costs

Your product has a learning curve that causes early cancellations

Your chargeback ratio is approaching monitoring thresholds

This doesn't make sense when:

You're seeing patterns suggesting organized fraud

Refund requests concentrate around specific features (might indicate a product problem worth fixing)

The same customers repeatedly request refunds

The goal isn't to eliminate all refunds—it's to make refunds easy enough that customers never feel the need to involve their bank.

Building Your Billing Support Playbook

Bring all of this together into a playbook your team can actually use:

Tier 1: Immediate refund authority

Transactions under [your threshold, e.g., $100]

First refund request from customer

Request made within [your window, e.g., 30 days]

Tier 2: Supervisor approval required

Transactions over threshold

Second+ refund request from same customer

Requests outside standard window

Customer mentions bank dispute

Tier 3: Finance escalation required

Customer has initiated chargeback

Suspected fraud patterns

System billing errors

For all tiers:

Capture evidence pack before closing ticket

Use approved response templates

Log outcome in CRM with evidence location noted

Your Next Step

Getting billing support right requires consistent processes, trained team members, and enough bandwidth to respond quickly. For many small SaaS companies, that's a lot to maintain alongside everything else.

If billing complaints are eating into time you should spend on product development or growth, it might be time to bring in support specialists who can handle these conversations with clear escalation routes to your finance team.

Book a call with Evergreen Support to discuss how outsourced email support with dedicated billing macros and escalation protocols could work for your business. We'll build the playbook together.

Frequently Asked Questions

What's the typical chargeback fee for SaaS companies?Most payment processors charge between $15-25 per chargeback, regardless of whether you win or lose the dispute. This is on top of losing the transaction amount if the dispute is decided against you. Some high-risk processors charge more. The fee alone makes chargebacks significantly more expensive than processing a refund for the same amount.

How long do I have to respond to a chargeback?You typically have 7-21 days to submit evidence for a chargeback dispute, depending on the card network and reason code. However, gathering evidence becomes much harder as time passes. That's why capturing documentation at the time of the original support interaction matters so much—you'll have everything ready when the deadline hits.

Should support teams be authorized to issue refunds without approval?For most SaaS companies, giving front-line support authorization to issue refunds up to a reasonable threshold (often $50-150) speeds resolution and prevents escalation. The key is clear guidelines about when supervisor approval is required and robust logging so finance has visibility into refund patterns.

How do I know if a chargeback is legitimate fraud versus friendly fraud?Legitimate fraud typically involves stolen card information and little to no product usage. Friendly fraud usually shows signs that the legitimate cardholder signed up: verified email, product usage, previous support interactions, or login history. Your evidence pack should make this distinction clear when building your dispute response.

What's the best way to train support teams on billing issues?Start with clear scripts and escalation triggers documented in an accessible playbook. Practice with real scenarios from your own ticket history. Review billing tickets as a team monthly to spot patterns and refine responses. Most importantly, explain why these procedures matter—when support understands the business impact of chargebacks, they handle billing issues more carefully.

About Evergreen Support

Evergreen Support provides US-based email support for small SaaS and ecommerce businesses. Our team handles billing inquiries, refund requests, and support escalations with established processes designed to protect your revenue and maintain your payment processing standing. We work as an extension of your team—learning your product, matching your brand voice, and following your escalation protocols.

Works Cited

[1] Chargebacks911 — "The True Cost of Chargebacks." https://chargebacks911.com/chargebacks/

[2] Stripe — "Billing Descriptors." https://stripe.com/docs/payments/account/statement-descriptors

[3] Visa — "Compelling Evidence 3.0 for Fraud Disputes." https://www.visa.com/

[4] Mastercard — "Excessive Chargeback Program." https://www.mastercard.com/